Beyond the Yield Curve: How Demographics and Technology Are Shaping the Next Decade of Bond Markets

The traditional yield curve can often be misleading. This analysis introduces a new model that looks beyond simple inversion to provide a clearer, more accurate forecast for financial markets. We will explore how the deep, structural forces of demographics and technology are fundamentally reshaping the next decade of bond markets.

The future of the global bond market is being fundamentally reshaped by two tectonic forces: the profound divergence of global demographics and the exponential advance of technology. For senior executives and portfolio managers at the world’s leading financial institutions, continuing to anchor strategy in the old paradigms is not just a missed opportunity—it is a critical failure of foresight. The winning strategy for the next decade demands a pivot, moving beyond the noise of cyclical data to build a new framework centered on understanding these deep, structural drivers. This is the only path to generating sustainable alpha and building resilient portfolios for a new era.

Force 1: The Great Demographic Rebalancing

The most predictable, yet most underestimated, force is the deep chasm opening between the demographic profiles of developed and emerging nations. This is not a subtle shift; it is a seismic rebalancing of savings, capital demand, and economic potential.

The Developed World’s Safe Asset Imperative

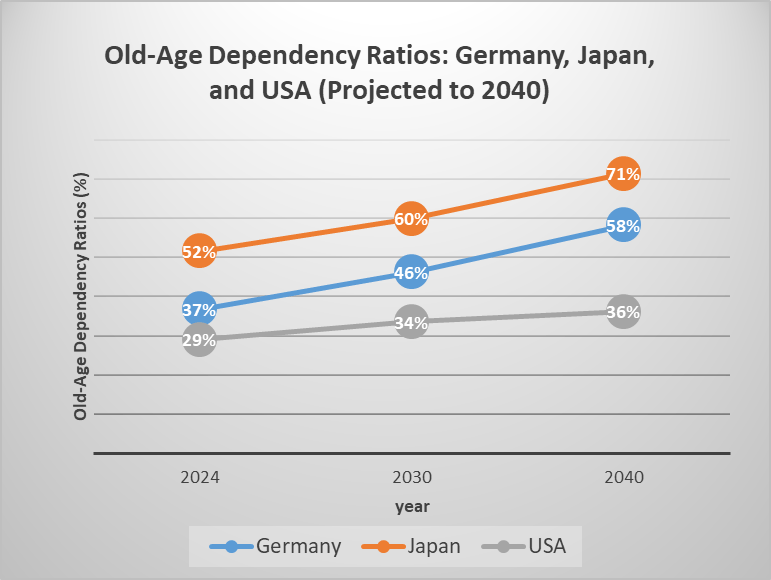

In the G7 nations, a powerful demographic transition is locking in decades of demand for safe, income-generating assets. Aging populations are transforming these economies into global savings engines. Projections show a stark reality: by 2040, Japan’s old-age dependency ratio is set to hit a staggering 71.3%, meaning fewer than 1.4 working-age individuals will support each elderly person. Germany faces a similar trajectory, with its dependency ratio projected to surge by over 21 percentage points to 58.2% in the same period.

This demographic reality creates what economists have termed the “savings glut of the old.” As PIMCO notes in its 2025 Secular Outlook, these headwinds are a key reason the firm anticipates maintaining more overweight duration positions. The structural demand from aging populations, which prioritize capital preservation, creates a massive, inelastic pool of capital seeking the safety of high-quality government and corporate bonds. Research from the OECD confirms the direct link: a 1 percentage point increase in the old-age dependency ratio correlates with a 0.2-0.3 percentage point decline in national savings rates, contributing directly to the fall in real interest rates over the past three decades. This isn’t a cycle; it’s a structural anchor on yields.

Emerging Markets: The Engine of Capital Demand

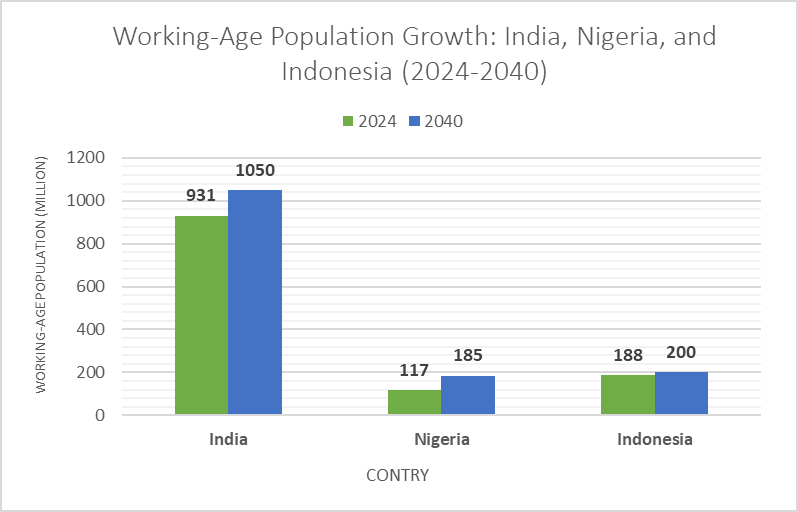

In stark contrast, a powerful “demographic dividend” is unfolding across South Asia and Africa. Nations like India, Nigeria, and Indonesia are entering their peak productive years. Nigeria’s working-age population is projected to explode by over 58% by 2040, while India will add 119 million new workers.

This youth bulge creates an insatiable appetite for capital. These economies need to build—roads, grids, cities, and schools. The World Bank estimates that emerging markets require an astonishing $5.4 trillion in annual investment by 2030 for the climate transition alone, a figure that dwarfs their domestic savings capacity. As BlackRock highlights in its “Mega Forces” framework, this “demographic divergence” is creating structural shifts that are not yet fully priced into markets. For astute bond investors, this translates into a historic opportunity. The financing gap in high-growth emerging markets will be filled by global capital, offering compelling yield opportunities in everything from sovereign debt to targeted infrastructure bonds.

Force 2: Technology’s Dual Disruption

The second structural force is technology, which is simultaneously creating new, multi-trillion-dollar asset classes and revolutionizing how credit risk itself is measured and managed.

The Trillion-Dollar Green Transition

The global energy transition represents the largest capital reallocation in history, and its primary financing vehicle is the bond market. The green bond market has experienced explosive growth, surging from just $11 billion in 2014 to over $570 billion in annual issuance by 2024—a compound annual growth rate of 63.9%. The cumulative sustainable debt market has already reached $6.9 trillion.

This is not a niche segment; it is becoming the market. Europe has led the way, accounting for over half of global green bond issuance, spurred by regulatory drivers like the EU Green Bond Standard. But the growth is global, with emerging market green bond issuance surging 45% to $209 billion in 2023. As BloombergNEF analysis shows, the world needs to invest $2.8 trillion annually through 2030 to meet climate goals. This demand ensures a deep and liquid market for green and sustainable debt for decades to come, offering investors the ability to finance the future while capturing potential “greeniums.”

The AI Revolution in Risk Analysis

“The battle for alpha in the next decade won’t be fought over basis points, but over petabytes,” notes a former Head of Quantitative Strategy. “The question is no longer who has the best economists, but who has the best data scientists.”

The quiet revolution in risk analysis is complete. Artificial intelligence and alternative data have rendered traditional credit models obsolete, creating a new frontier for generating alpha. The adoption of AI/ML in credit risk management has skyrocketed, jumping from 15% of financial institutions in 2020 to a projected 85% by 2025.

The results are undeniable. Machine learning models now achieve over 90% accuracy in credit scoring, far surpassing the 60-70% accuracy of legacy statistical models. Leading institutions are already deploying this advantage. Moody’s AI-powered Research Assistant has cut financial analysis time by 30%, while S&P Global’s new CreditCompanion™ platform leverages large language models to provide comparative credit analysis in seconds.

This is more than an efficiency gain; it is a fundamental shift in information advantage. AI models process vast streams of alternative data—from satellite imagery and supply chain logs to real-time financial flows—to identify risk signals months before traditional rating methods. For portfolio managers, this means the ability to anticipate downgrades, identify mispriced risk, and gain a decisive edge. The development of Explainable AI (XAI) is already addressing regulatory concerns around model transparency, paving the way for mainstream adoption.

The CIO’s Mandate: A New Framework for a New Reality

The convergence of these forces—demographic divergence and technological disruption—obliterates the old playbook. Relying solely on interest rate forecasts in a world being reshaped by such powerful structural tides is like navigating a hurricane with only a barometer.

The winning strategy for the next decade requires a fundamental pivot. Asset managers must move beyond chasing cyclical data points and build a new, robust framework centered on these deep structural forces. This means:

- Integrating Demographic Analysis: Asset allocation must be explicitly tied to demographic trajectories. This involves balancing the demand for safe, long-duration assets from aging developed nations with strategic allocations to the high-growth, capital-hungry emerging markets benefiting from a demographic dividend.

- Embracing Technology-Driven Alpha: Firms must invest in AI-enhanced credit assessment capabilities. The edge in fixed-income will no longer come from having a better macro forecast, but from having a superior ability to process alternative data and identify granular, bottom-up risk that legacy models miss.

- Strategic Allocation to Thematic Debt: Portfolios must reflect the massive capital needs of the future. A meaningful, strategic allocation to green bonds and sustainable infrastructure debt is no longer an ESG-driven niche play; it is a core component of capturing long-term, risk-adjusted returns.

The leaders of the next decade—the BlackRocks and PIMCOs of tomorrow—will be those who recognize this paradigm shift today. The currents of demographics and technology are pulling the market into a new and unfamiliar territory. The time to build a new map is now.

Leave a comment