The institutional fixed income market is ignoring a structural fiscal cliff. While consensus focuses on short term central bank policy, the real risk lies in the massive refinancing requirements of G7 economies. The US fiscal trajectory presents a 100 basis point repricing risk for 10 year government bonds that most models fail to capture.

The Refinancing Cliff

The US government owes 38 trillion dollars. Debt to GDP now exceeds 120 percent. This trajectory is unsustainable. The critical issue is the maturity ladder. Approximately 25 to 30 percent of this debt matures annually. This requires the government to roll over 9 to 11 trillion dollars every year at current market rates.

If 10 year Treasury yields rise by 80 basis points, annual interest costs increase by 72 billion dollars. Over a decade, this adds 720 billion dollars in cumulative costs. We are approaching a threshold where interest payments will exceed tax revenue. This math is fundamental and unavoidable.

The Breakdown of the Correlation Hedge

For 40 years, investors treated bonds as a reliable hedge against equity volatility. This negative correlation is breaking. In a fiscal stress scenario, inflation concerns and debt supply pressure cause bond prices and equity prices to fall together.

Bonds are transitioning from safety assets to risk assets. When the market questions fiscal sustainability, duration no longer provides protection. This shift destroys the foundation of the traditional 60/40 portfolio. You must recognize that government debt yields are now a source of systemic risk rather than a refuge.

Term Premium Repricing

Term premiums remain at historical lows. Investors receive minimal compensation for holding long duration government debt. This mispricing ignores fiscal deterioration and inflation uncertainty.

We expect a sharp repricing of the term premium. The 10 year yield will likely rise 50 to 100 basis points independent of Federal Reserve policy. This shift will happen even if the central bank attempts to ease. The supply of new debt will simply overwhelm demand at current yield levels.

Actionable Strategy for the CIO

You must reduce duration exposure immediately. Long dated bonds in the 10 to 30 year range offer an unfavorable risk reward profile. You should rotate capital into intermediate maturities of 5 to 7 years. This position provides a better carry with significantly lower repricing risk.

Monitor the term premium spread constantly. A material widening signals the start of a systemic repricing event. You should also consider emerging market local currency bonds as a diversifier against US dollar fiscal pressure.

The window for proactive positioning is narrow. By the time fiscal math becomes a mainstream headline, the repricing will be complete. You must act before the consensus realizes the risk.

How a Three-Act Crisis Forged a Fractured, Two-Tier Financial System

For decades, global capital markets have rested on a fundamental assumption: the U.S. Treasury market is the ultimate risk-free haven, underpinned by limitless liquidity. This assumption, once the bedrock of portfolio construction, is now a perilous illusion. Beneath a veneer of superficial stability, bond market liquidity is not evolving—it is dying, replaced by a synthetic ecosystem that fundamentally redefines systemic risk.

Act I: The Tremor – A Microstructural Warning Shot

The deterioration began with a profound tremor in the market’s core infrastructure. The April 2025 Treasury market liquidity crisis, following a surprise tariff announcement, was not a fleeting anomaly but a clear warning shot. The Federal Reserve Bank of New York documented a severe breakdown, with key metrics rapidly nearing or exceeding the stress levels of the March 2023 banking crisis.

The damage was precise and alarming:

Bid-ask spreads for longer-term off-the-run Treasuries and TIPS “jumped quickly and approximately doubled in size.”

Market depth in the benchmark 10-year security “declined to about one-quarter of recent levels.”

The TIPS liquidity premium surged by 30 basis points in a single week—”a magnitude highly unusual in such a short time.”

Most unsettling was the breakdown in traditional safe-haven behavior. While Treasuries initially rallied, the effect was short-lived. Yields began climbing in subsequent sessions as government bonds fell in value alongside equities. This decoupling exposed a fragility that the Federal Reserve’s own research had presciently warned of just months earlier, noting that reduced “market depth” critically increases dependence on the “prompt replenishment of resting orders”—a dependency that proved tragically fragile.

This microstructural fragility, while alarming, was merely a symptom. The true danger lay in the fact that the system’s primary shock absorber was about to disappear.

Act II: The Drain – A System Without a Safety Net

The second act of the crisis was the exhaustion of the Federal Reserve’s overnight reverse repo (ON RRP) facility. By August 2025, cash flowing into the facility had fallen to near-zero for the first time in years. This was not a technical normalization; it was the removal of a crucial systemic stabilizer. As Bloomberg noted, with the RRP’s cushion gone, repo markets became “more vulnerable to swings in Treasury issuance.”

The NY Fed’s own research had identified four critical early warning signals of reserve scarcity, all of which flashed red in early 2025. The consensus among analysts like JP Morgan was clear: the exhaustion of the ON RRP is not a sign of health, but “the removal of a systemic stabilizer.” With Treasury issuance elevated and M2 growth stagnant, the domestic financial system was left exposed and brittle.

Into this void of traditional liquidity and dwindling reserves, a new, powerful, and poorly understood force began to proliferate, promising a solution while masking a deeper fragmentation.

Act III: The Proliferation – A Synthetic Solution with Systemic Flaws

The third act is the explosive, and largely opaque, expansion of a synthetic market. The tokenized government bond market surged past $6 billion in 2025, led by BlackRock’s BUIDL and Franklin Templeton’s BENJI. The broader tokenized asset market hit $24 billion, with projections nearing $30 trillion by 2034.

The Bank for International Settlements (BIS) has embraced this shift, with its “Project Agorá” testing a “trilogy of tokenized central bank reserves, commercial bank money and government bonds.” Yet, even the BIS admits that current structures “fall short” and face “significant challenges,” including fragmentation.

Crucially, academic research from September 2025 confirms these fears. The paper, “Tokenize Everything, But Can You Sell It?”, documented that despite the promise of 24/7 markets, “most RWA tokens exhibit low trading volumes, long holding periods, and limited investor participation.” The reasons cited are structural: regulatory gating, custodial concentration, and a lack of decentralized trading venues. This new tier, built to solve a problem, has introduced an entirely new architecture of risk.

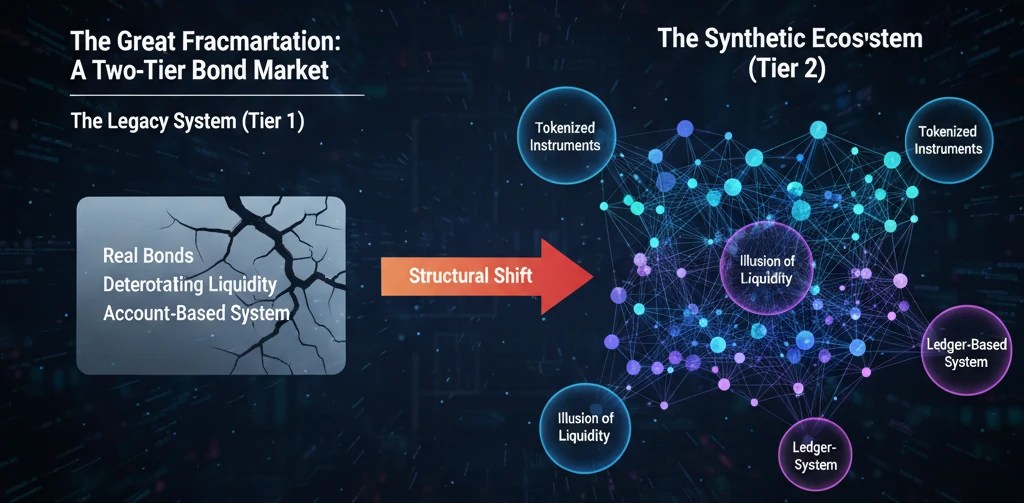

The Consequence: A Two-Tier System and the Fragmentation of Finance

The convergence of these three crises has forged an unprecedented two-tier system in global fixed income.

The First Tier, the legacy account-based system, is a shrinking core of “real” bonds suffering from deteriorating liquidity. The stress events of April 2025 are a preview of its future: a brittle and unpredictable market where depth can vanish instantly.

The Second Tier, the new ledger-based system, is an expanding universe of synthetic instruments. It offers the illusion of perpetual accessibility but is plagued by structural barriers, valuation opacity, and concentrated points of failure.

The global fixed income market is no longer a monolith. It is fragmenting into distinct, often incompatible, liquidity architectures. What constitutes “liquidity” in one tier may not translate—or even exist—in the other, creating systemic disconnects that regulatory frameworks are unequipped to handle.

The CIO’s Dilemma: Navigating a World Without a True Haven

The empirical evidence is conclusive: traditional bond market liquidity is not merely evolving; it is dying. It is being supplanted by a synthetic ecosystem that generates an illusion of liquidity while concentrating systemic risk in ways that make previous financial crises appear almost predictable. The April liquidity event, the near-zero RRP, and the fragmented growth of tokenized instruments are not isolated data points. They are symptoms of a profound, irreversible structural transformation.

For Chief Investment Officers and portfolio managers, this necessitates an immediate re-evaluation of established models. The frameworks built upon a robust sovereign bond market are becoming obsolete. The questions now are not merely about managing duration or credit, but about the very nature of liquidity itself: How do strategies adapt to a bifurcated market where traditional depth is compromised and synthetic alternatives carry unquantified risks?

For decades, the fixed income market has been the bedrock of global finance, yet it operates on infrastructure that can only be described as antiquated. This “antiquated plumbing” has created deep-seated, structural problems, particularly chronic illiquidity and high transaction friction in key sectors. Recent data from 2024-2025 starkly illustrates this reality: the average transaction cost for municipal bonds has soared to approximately 50 basis points, a persistent elevation that has outlasted multiple market crises. Odd-lot trades in this sector face even higher spreads of 56 basis points. Meanwhile, the burgeoning $2.5 trillion private credit market faces its own crisis of opacity and illiquidity, with no secondary market exit options for most investors.

Against this backdrop, the tokenization of fixed income is emerging not as a mere technical upgrade, but as a fundamental infrastructure shift. It is a revolution poised to solve the market’s two historical weaknesses, unlocking unprecedented efficiency, democratizing access, and enabling a new wave of product innovation. For institutional investors, ignoring this transformation is no longer an option.

Tokenization Explained: The “Digital Twin”

At its core, tokenization is the process of creating a “digital twin” of a real-world asset, such as a bond, on a blockchain. This digital token represents legal ownership of the underlying security. Each token is a programmable, cryptographically secure digital record that contains all the rights, features, and legal obligations of the traditional bond. This digital representation lives on a distributed ledger, a shared and immutable database that allows all authorized participants to see the same version of the truth simultaneously, eliminating the need for complex, siloed reconciliation processes.

The Primary Solution: Solving the Liquidity Puzzle

The most profound impact of tokenization is its ability to solve the market’s chronic liquidity problem, primarily through fractionalization. By creating a digital representation of a bond, issuers can divide it into smaller, more affordable units. This is not a theoretical benefit; it is already happening.

Platforms like BondbloX, the world’s first regulated fractional bond exchange, are breaking down traditional bonds with 200,000 minimums into $1,000 fractional units, enabling 200 times greater diversification. Similarly, Singapore’s **OCBC Bank** now offers customized tokenized bonds in S$1,000 denominations, a stark contrast to the traditional S250,000 minimums.

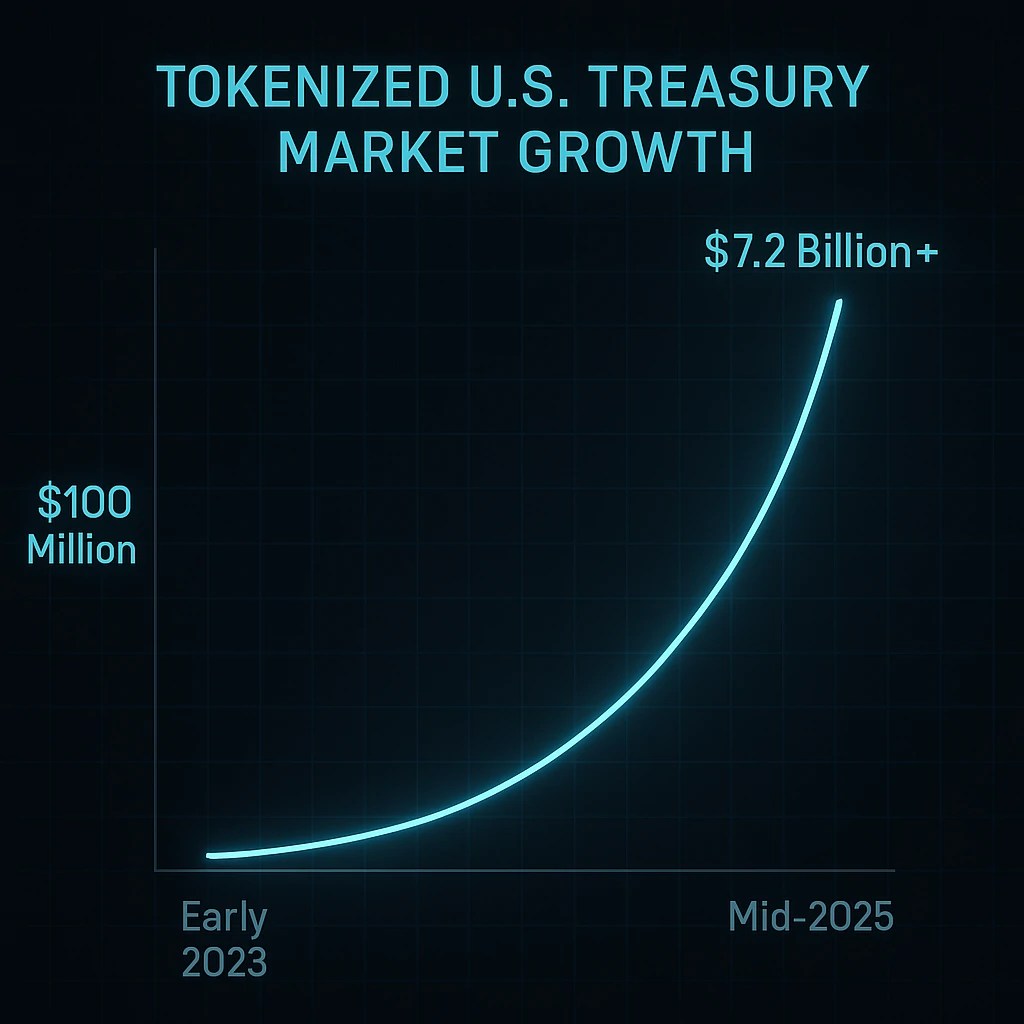

This fractionalization dramatically expands the pool of potential investors beyond large institutions, bringing new capital and liquidity into previously inaccessible markets. The early success in the most liquid asset class—U.S. Treasuries—serves as a powerful proof of concept. The tokenized Treasury market has surged from under $100 million in early 2023 to over $7.2 billion by mid-2025, with institutional giants like BlackRock, Franklin Templeton, and Fidelity all launching tokenized money market funds.

Beyond Liquidity: Efficiency and Innovation

While enhanced liquidity is the headline benefit, the secondary advantages of tokenization are equally revolutionary.

1. Atomic Settlement and Operational Efficiency:

The traditional bond market is plagued by multi-day settlement cycles (T+2 or longer), which introduce counterparty risk and operational friction. Tokenization enables “atomic settlement,” where the transfer of the asset and the payment occur simultaneously and instantly (T+0). The results from institutional pilots are compelling:

Goldman Sachs, through its GS DAP platform, achieved same-day (T+0) settlement for a €100 million digital bond issued by the European Investment Bank (EIB).

HSBC’s Orion platform reduced the settlement cycle for a multi-currency digital bond from T+5 to T+1, a dramatic four-day improvement.

This efficiency eliminates settlement risk, automates manual processes, and significantly reduces the costs associated with intermediaries like clearinghouses and custodians.

2. Product Innovation through Smart Contracts:

Tokens are programmable. The terms and conditions of a bond can be embedded into a smart contract, which automatically executes actions like coupon payments and maturity redemptions. This automation eliminates errors and operational overhead. More importantly, it opens the door to unprecedented product innovation. Imagine complex structured products with automated, rules-based triggers or ESG bonds where compliance metrics are automatically tracked and reported on-chain. JPMorgan’s Project Guardian demonstrated this potential by using tokenization to enable mass-scale, customized portfolio construction across traditional and alternative assets, a task previously unfeasible for the wealth management industry.

A Balanced View: The Hurdles to Widespread Adoption

Despite the clear potential, the path to a fully tokenized fixed income market is not without significant obstacles. The primary challenges are regulatory and technical.

The regulatory landscape remains fragmented and uncertain. In the U.S., the SEC under Chairman Paul Atkins has launched “Project Crypto” to create a more crypto-friendly framework, yet fundamental questions persist. As Commissioner Hester Peirce stated:

“tokenized securities are still securities”

This means they are subject to all existing laws. Key hurdles include:

Custody Requirements: The SEC’s Customer Protection Rule (Rule 15c3-3) was not designed for digital assets, creating uncertainty for broker-dealers on how to custody tokens compliantly.

Transfer Agent Rules: It remains unclear whether a blockchain ledger can serve as the authoritative record of ownership, and who—from software developers to validators—might be deemed a transfer agent.

Cross-Border Fragmentation: The European Union’s DLT Pilot Regime has seen slow adoption, while the UK is developing its own sandbox. This lack of international harmony creates significant compliance costs for global institutions.

These legal ambiguities force many innovative projects offshore and slow the pace of institutional adoption.

The New Competitive Landscape: Winners and Losers

This technological shift will create clear winners and losers across the financial ecosystem:

Investment Banks: Institutions like Goldman Sachs, JPMorgan, and HSBC are moving from pilots to building out proprietary platforms (GS DAP, Kinexys, Orion). Their role will evolve from intermediaries to technology providers, offering tokenization-as-a-service and creating new digital market infrastructure.

Asset Managers: The ability to offer fractionalized access to illiquid assets like private credit and to build highly customized, automated portfolios will become a key competitive differentiator.

Issuers: Tokenization offers access to a broader, more global investor base and significantly lower issuance costs, making it particularly attractive for smaller issuers in fragmented markets like municipal finance.

Conclusion & Outlook: The Trillion-Dollar Opportunity

The tokenization of fixed income is not a question of if, but when and how fast. The inefficiencies of the current system are too great to ignore, and the benefits of the new infrastructure are too compelling. While regulatory hurdles will ensure the transition is gradual, the direction of travel is clear.

Forecasts for the size of the tokenized asset market by 2030 vary widely, but the scale is consistently monumental. The Boston Consulting Group (BCG) projects a $9.4 trillion market, McKinsey offers a more conservative $2 trillion estimate, while Citi forecasts $4-5 trillion. The median forecast of a nearly $10 trillion market represents a potential 40-fold increase from today’s levels.

This is more than an incremental improvement; it is the dawn of a new, more efficient, and more accessible financial architecture. The institutions that invest in understanding and adopting this technology today will be the ones that define the future of capital markets.

The global ESG bond market has firmly established itself as a cornerstone of modern finance. With issuance hitting the symbolic $1 trillion mark for the second time in 2024, the sheer scale of this market is undeniable. Green bonds continue to dominate, accounting for approximately $672 billion of the total, a 9% year-over-year increase, reflecting an unyielding demand for climate-focused investments.

Yet, this explosive growth has brought with it a significant challenge: the pervasive risk of “greenwashing.” For the informed investor, navigating this landscape requires more than just a thematic preference for “green” projects. The key to successful ESG bond investing, and the core argument of this article, is the application of a rigorous, analytical framework that moves beyond labels to measure real-world impact, mitigate reputational risk, and ultimately, unlock sustainable financial outperformance, or “alpha.”

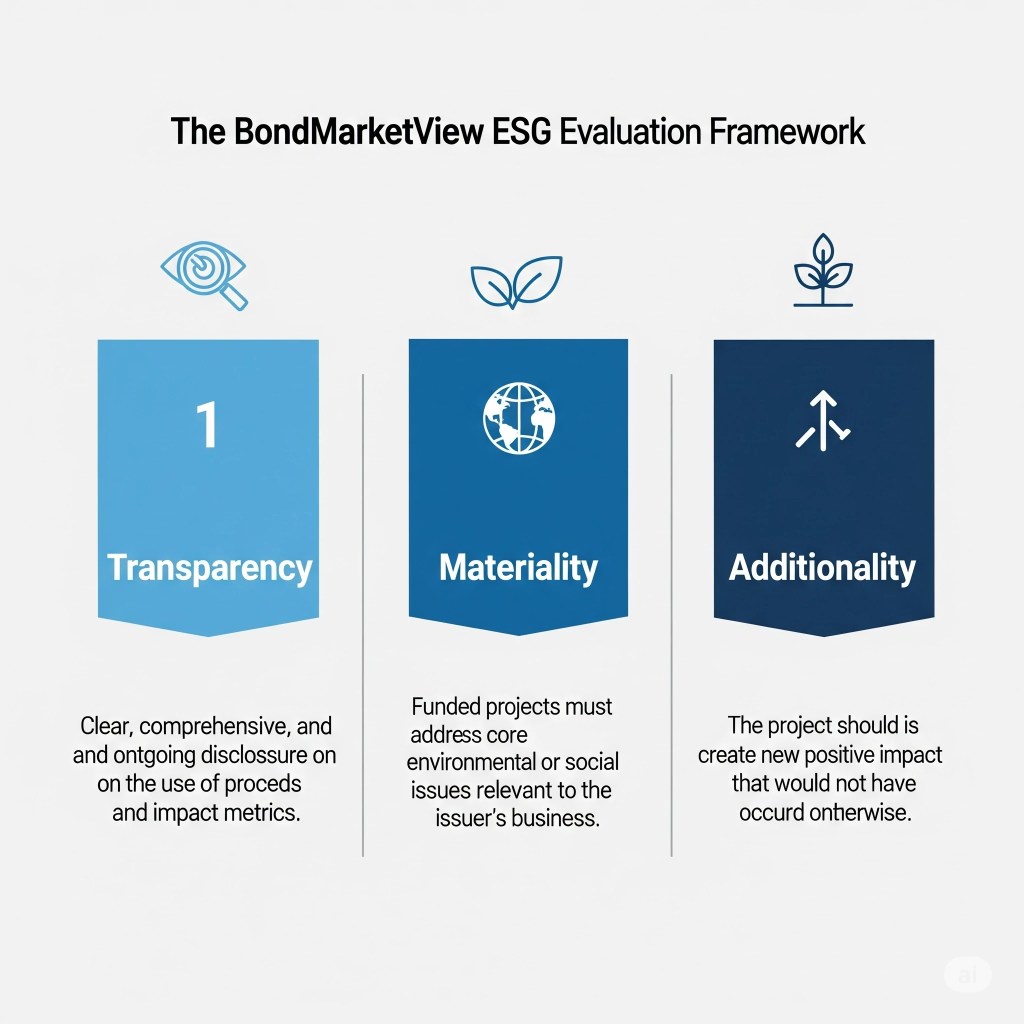

The BondMarketView Framework: A Disciplined Approach to ESG Evaluation

In a market crowded with issuances of varying quality, a disciplined evaluation framework is essential. At BondMarketView, we advocate for a three-pronged approach focused on Transparency, Materiality, and Additionality.

Transparency: This goes beyond simply labeling a bond “green” or “social.” It requires clear, comprehensive, and ongoing disclosure. Investors should demand granular reporting on the use of proceeds, the specific projects being funded, and the metrics used to track their impact. Post-issuance reporting is not a “nice-to-have”; it is a critical component of a credible ESG bond.

Materiality: The funded projects must address environmental or social issues that are material to the issuer and its stakeholders. For example, a green bond from a utility company focused on renewable energy infrastructure has high materiality. In contrast, a bond from the same company to fund energy-efficient lighting in its corporate offices, while positive, is less material to its core business and overall environmental impact.

Additionality: This is perhaps the most crucial and often overlooked element. A high-quality ESG bond should fund projects that would not have been undertaken otherwise. It should create additional positive impact, not simply refinance existing “green” assets. This concept challenges investors to ask the tough question: Is this bond truly creating a more sustainable future, or is it merely a marketing exercise?

A Tale of Two Bonds: A Comparative Case Study

The difference between a high-quality ESG issuance and a controversial one often lies in the rigor of its framework.

The Gold Standard:

Recent examples of successful ESG bonds highlight the importance of our framework. The New Development Bank’s (NDB) USD 1.25 billion green bond, issued in November 2024, is a case in point. Its success is underpinned by NDB’s Sustainable Financing Policy Framework, which provides a robust and transparent process for project selection, evaluation, and reporting. Similarly, the Societe des Grands Projets’ (SdGP) EUR 1 billion green bond for the Grand Paris Express metro project, which was 17 times oversubscribed, benefits from certification under the Climate Bonds Standard, a globally recognized benchmark for best practices. The Dominican Republic’s debut sovereign green bond also stands out. The USD 750 million issuance, which was six times oversubscribed, funds a range of clean energy, transportation, and waste management projects, and was priced approximately 15 basis points cheaper than comparable non-thematic issues, signaling strong market confidence.

The “Greenwashing” Trap:

On the other end of the spectrum are bonds that, while labeled “green,” face criticism for a lack of transparency and impact. While specific “infamous” bonds are often hard to pinpoint in a given year, a pattern of “greenwashing” concerns has emerged, particularly in some rapidly growing but less regulated markets. Analysts have pointed to instances where a significant portion of green bond proceeds, in some cases up to 50%, have been allocated to general working capital or projects with questionable environmental benefits. This misallocation, coupled with a lack of alignment with international standards like the Climate Bonds Initiative, erodes investor confidence and undermines the integrity of the market. These examples highlight the critical importance of due diligence and a skeptical, analytical approach.

From Impact to Alpha: The Financial Case for High-Quality ESG

The link between robust ESG practices and financial performance is no longer a matter of debate; it is a data-driven reality. Recent academic studies and financial reports from 2024 and 2025 provide compelling evidence of this correlation.

A July 2024 study of publicly listed Chinese companies found that strong environmental and social ESG practices significantly reduce corporate credit risk. Another 2024 study of European banks confirmed that ESG factors have a tangible impact on credit ratings from major agencies. For portfolio managers, the implications are clear: a 2024 study of corporate bond portfolios from 2013-2020 found that portfolios with the highest ESG scores were significantly less exposed to credit risk.

The story doesn’t end with risk mitigation. A 2025 study of Chinese A-share listed companies from 2009 to 2022 demonstrated that better ESG performance significantly boosts financial returns. This aligns with broader meta-analyses, with approximately 58% of studies showing a positive relationship between ESG and financial returns.

Implications for Investors

The evolving ESG bond market presents different opportunities and challenges for various investor types:

For the Pension Fund Manager: The long-term, liability-driven nature of pension funds aligns perfectly with the risk mitigation characteristics of high-quality ESG bonds. The focus should be on building a core holding of highly-rated, transparent, and impactful bonds that can provide stable, long-term returns.

For the Active Credit Manager: The inefficiencies and information asymmetries in the ESG bond market create opportunities for alpha generation. By applying a rigorous analytical framework, active managers can identify mispriced bonds and avoid those with high “greenwashing” risk.

For the Retail Investor: The proliferation of ESG-focused ETFs and mutual funds has made this market more accessible. However, retail investors should look beyond the fund’s name and examine its methodology for selecting bonds. A fund that prioritizes transparency, materiality, and additionality is more likely to deliver on both its impact and financial goals.

Conclusion & Outlook

The ESG bond market has matured from a niche segment to a mainstream asset class. As the market continues to evolve, the ability to distinguish between genuine impact and “greenwashing” will be the defining characteristic of a successful investment strategy. The data is clear: a disciplined, analytical approach to ESG bond investing, focused on transparency, materiality, and additionality, not only contributes to a more sustainable future but also leads to superior, risk-adjusted returns.

Looking ahead, we are watching several key trends. Regulatory scrutiny is set to increase, with a greater push for standardized disclosure and reporting requirements. The development of more sophisticated impact measurement methodologies will also be crucial. And as the market continues to grow, the ability to source high-quality, impactful projects will become an increasingly important differentiator. For the astute strategist, the ESG bond market is not just about investing in a better world; it’s about investing intelligently in the world of tomorrow.

Beyond the Yield Curve: How Demographics and Technology Are Shaping the Next Decade of Bond Markets

The traditional yield curve can often be misleading. This analysis introduces a new model that looks beyond simple inversion to provide a clearer, more accurate forecast for financial markets. We will explore how the deep, structural forces of demographics and technology are fundamentally reshaping the next decade of bond markets.

The future of the global bond market is being fundamentally reshaped by two tectonic forces: the profound divergence of global demographics and the exponential advance of technology. For senior executives and portfolio managers at the world’s leading financial institutions, continuing to anchor strategy in the old paradigms is not just a missed opportunity—it is a critical failure of foresight. The winning strategy for the next decade demands a pivot, moving beyond the noise of cyclical data to build a new framework centered on understanding these deep, structural drivers. This is the only path to generating sustainable alpha and building resilient portfolios for a new era.

Force 1: The Great Demographic Rebalancing

The most predictable, yet most underestimated, force is the deep chasm opening between the demographic profiles of developed and emerging nations. This is not a subtle shift; it is a seismic rebalancing of savings, capital demand, and economic potential.

The Developed World’s Safe Asset Imperative

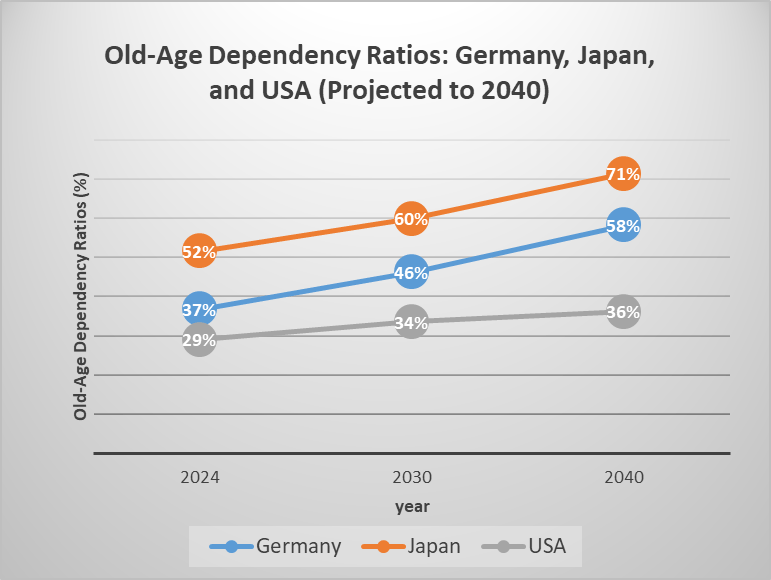

In the G7 nations, a powerful demographic transition is locking in decades of demand for safe, income-generating assets. Aging populations are transforming these economies into global savings engines. Projections show a stark reality: by 2040, Japan’s old-age dependency ratio is set to hit a staggering 71.3%, meaning fewer than 1.4 working-age individuals will support each elderly person. Germany faces a similar trajectory, with its dependency ratio projected to surge by over 21 percentage points to 58.2% in the same period.

Fig. 1: Diverging aging trajectories in major economies through 2040. Source: BondMarketView analysis.

This demographic reality creates what economists have termed the “savings glut of the old.” As PIMCO notes in its 2025 Secular Outlook, these headwinds are a key reason the firm anticipates maintaining more overweight duration positions. The structural demand from aging populations, which prioritize capital preservation, creates a massive, inelastic pool of capital seeking the safety of high-quality government and corporate bonds. Research from the OECD confirms the direct link: a 1 percentage point increase in the old-age dependency ratio correlates with a 0.2-0.3 percentage point decline in national savings rates, contributing directly to the fall in real interest rates over the past three decades. This isn’t a cycle; it’s a structural anchor on yields.

Emerging Markets: The Engine of Capital Demand

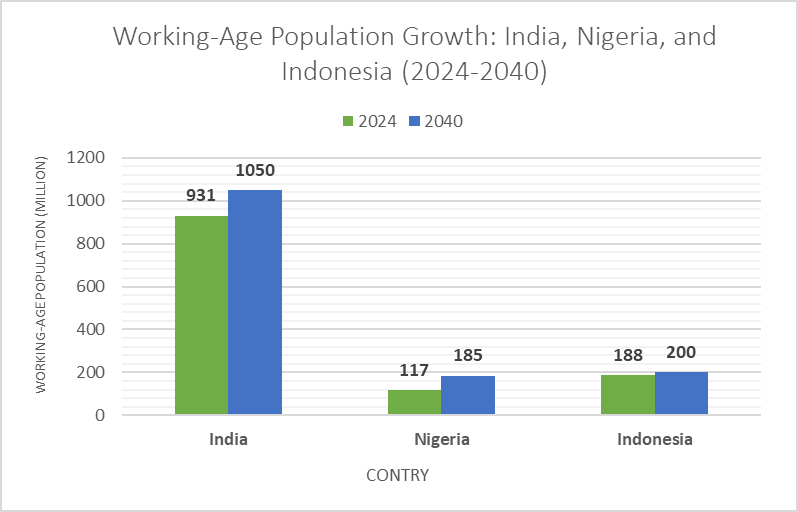

In stark contrast, a powerful “demographic dividend” is unfolding across South Asia and Africa. Nations like India, Nigeria, and Indonesia are entering their peak productive years. Nigeria’s working-age population is projected to explode by over 58% by 2040, while India will add 119 million new workers.

Fig. 2: The ‘demographic dividend’ in key emerging markets, illustrating the immense growth in the working-age population which fuels capital demand. Source: BondMarketView analysis of UN and World Bank data.

This youth bulge creates an insatiable appetite for capital. These economies need to build—roads, grids, cities, and schools. The World Bank estimates that emerging markets require an astonishing $5.4 trillion in annual investment by 2030 for the climate transition alone, a figure that dwarfs their domestic savings capacity. As BlackRock highlights in its “Mega Forces” framework, this “demographic divergence” is creating structural shifts that are not yet fully priced into markets. For astute bond investors, this translates into a historic opportunity. The financing gap in high-growth emerging markets will be filled by global capital, offering compelling yield opportunities in everything from sovereign debt to targeted infrastructure bonds.

Force 2: Technology’s Dual Disruption

The second structural force is technology, which is simultaneously creating new, multi-trillion-dollar asset classes and revolutionizing how credit risk itself is measured and managed.

The Trillion-Dollar Green Transition

The global energy transition represents the largest capital reallocation in history, and its primary financing vehicle is the bond market. The green bond market has experienced explosive growth, surging from just $11 billion in 2014 to over $570 billion in annual issuance by 2024—a compound annual growth rate of 63.9%. The cumulative sustainable debt market has already reached $6.9 trillion.

This is not a niche segment; it is becoming the market. Europe has led the way, accounting for over half of global green bond issuance, spurred by regulatory drivers like the EU Green Bond Standard. But the growth is global, with emerging market green bond issuance surging 45% to $209 billion in 2023. As BloombergNEF analysis shows, the world needs to invest $2.8 trillion annually through 2030 to meet climate goals. This demand ensures a deep and liquid market for green and sustainable debt for decades to come, offering investors the ability to finance the future while capturing potential “greeniums.”

The AI Revolution in Risk Analysis

“The battle for alpha in the next decade won’t be fought over basis points, but over petabytes,” notes a former Head of Quantitative Strategy. “The question is no longer who has the best economists, but who has the best data scientists.”

The quiet revolution in risk analysis is complete. Artificial intelligence and alternative data have rendered traditional credit models obsolete, creating a new frontier for generating alpha. The adoption of AI/ML in credit risk management has skyrocketed, jumping from 15% of financial institutions in 2020 to a projected 85% by 2025.

The results are undeniable. Machine learning models now achieve over 90% accuracy in credit scoring, far surpassing the 60-70% accuracy of legacy statistical models. Leading institutions are already deploying this advantage. Moody’s AI-powered Research Assistant has cut financial analysis time by 30%, while S&P Global’s new CreditCompanion™ platform leverages large language models to provide comparative credit analysis in seconds.

This is more than an efficiency gain; it is a fundamental shift in information advantage. AI models process vast streams of alternative data—from satellite imagery and supply chain logs to real-time financial flows—to identify risk signals months before traditional rating methods. For portfolio managers, this means the ability to anticipate downgrades, identify mispriced risk, and gain a decisive edge. The development of Explainable AI (XAI) is already addressing regulatory concerns around model transparency, paving the way for mainstream adoption.

The CIO’s Mandate: A New Framework for a New Reality

The convergence of these forces—demographic divergence and technological disruption—obliterates the old playbook. Relying solely on interest rate forecasts in a world being reshaped by such powerful structural tides is like navigating a hurricane with only a barometer.

The winning strategy for the next decade requires a fundamental pivot. Asset managers must move beyond chasing cyclical data points and build a new, robust framework centered on these deep structural forces. This means:

Integrating Demographic Analysis: Asset allocation must be explicitly tied to demographic trajectories. This involves balancing the demand for safe, long-duration assets from aging developed nations with strategic allocations to the high-growth, capital-hungry emerging markets benefiting from a demographic dividend.

Embracing Technology-Driven Alpha: Firms must invest in AI-enhanced credit assessment capabilities. The edge in fixed-income will no longer come from having a better macro forecast, but from having a superior ability to process alternative data and identify granular, bottom-up risk that legacy models miss.

Strategic Allocation to Thematic Debt: Portfolios must reflect the massive capital needs of the future. A meaningful, strategic allocation to green bonds and sustainable infrastructure debt is no longer an ESG-driven niche play; it is a core component of capturing long-term, risk-adjusted returns.

The leaders of the next decade—the BlackRocks and PIMCOs of tomorrow—will be those who recognize this paradigm shift today. The currents of demographics and technology are pulling the market into a new and unfamiliar territory. The time to build a new map is now.